If it seems like hurricane season has been getting worse, it’s because it has. Weather and climate disasters in the U.S. cost trillions in damage from 1980 to 2023, according to the National Oceanic and Atmospheric Administration, and storms continue to make historic benchmarks in losses.

Atlantic hurricane season runs from June to November, usually hitting its stride around mid-August through October. Before the next storm, read through this guide and talk to a AAA Insurance agent to make sure you, your family and your belongings are ready to weather the worst of it and bounce back better than ever.

Disclaimer: The content in this guide is intended for informational purposes only. In the case of an imminent hurricane, please defer to the advice of health and safety professionals.

Hurricane Readiness Basics

Take advantage of the calm long before a storm to plan for your family’s safety.

Sign Up for Storm Alerts

The Federal Emergency Management Agency’s (FEMA) mobile app will send you National Weather Service notifications on up to five locations and locate emergency shelters. Keep an eye on local news and weather reports as well.

Plan for Evacuation

State or local officials may issue evacuation notices in advance of dangerous storms. Check with your local departments of transportation or emergency management to familiarize yourself with your area’s evacuation routes and shelters. Keep your car’s gas tank at least half full – or your EV charged – and carry a kit of basic emergency supplies in your trunk.

If you have to leave your home on short notice, you’ll want some essentials for you and everyone in your family. FEMA recommends having an emergency go-bag ready with things like medications, food and water, clothing and a first-aid kit. Your bag should be easy to carry and kept where you can grab it quickly.

Remember to secure your home before leaving and check with neighbors who may need a ride.

Emergency Supply Checklist

An emergency preparedness kit can ensure you have what you need in case an extreme weather event causes a power outage or requires evacuation.

You can build an emergency stockpile over time but remember to replace items with a limited shelf life, like food and batteries.

- 1 gallon of water per person per day for at least three days.

- At least a three-day supply of nonperishable food.

- Battery or hand-crank radio and extra batteries.

- Flashlight with extra batteries.

- A whistle to signal for help.

- A portable phone charger.

- A first-aid kit.

- A wrench and/or pliers.

- Dust mask to filter contaminated air.

- Plastic sheeting and duct tape.

- Moist towelettes, garbage bags and plastic ties for personal sanitation.

- Can opener if your food kit contains cans.

- Local maps.

- Prescriptions and reading glasses.

- Infant formula and diapers.

- Food, water and medication for your pets.

- Important family documents, such as insurance policies and bank account records. Store these in a waterproof container.

- Sleeping bags or warm blankets.

- Cash and change.

- Complete change of clothing, including a long-sleeve shirt and long pants.

- A fire extinguisher.

- Matches in a waterproof container.

- Feminine and personal hygiene supplies.

- Paper cups, plates, plastic utensils and paper towels.

Establish a Communication Plan

Figure out how your family will stay in touch if you’re separated or lose power. You can choose an out-of-state contact for everyone to use and designate a meetup spot.

Staying Put

If you’re not ordered to evacuate, stay indoors, away from windows and glass doors. Never use a generator or gasoline-powered equipment indoors or in partially enclosed areas. Such equipment should be outside, 20 feet away from doors, windows and vents.

Ready Your Car

In addition to making sure your vehicle is fueled up and keeping an emergency kit handy, basic vehicle maintenance is important ahead of hurricane season, especially if you live in a coastal state where evacuations are more likely.

Car batteries typically have a three- to five-year lifespan. Call AAA for a battery inspection to ensure your car will start when you need it most; a battery service technician will come to your home or workplace to test your battery and, if needed, can replace your battery on the spot.

Visit a reputable repair shop to check your brakes, inspect your tires, assess fluids and hoses and replace your windshield wipers, if needed.

If you have an electric vehicle, you should also stay on top of basic car care and consider mapping out charging stations along evacuation routes ahead of time.

Ready Your Home

Powerful winds and floods are two of the greatest dangers presented by hurricanes. Ready your home by reinforcing doors, windows, walls and the roof. Depending on your risk, you may also want to consider long-term solutions like installing storm shutters and hurricane-proof doors.

You should bring loose, light objects like patio furniture and garbage cans inside and anchor objects you cannot bring inside, like grills. Trim or remove trees that are close enough to fall on buildings.

To prepare your home for heavy rains or flooding, keep gutters and drains free of debris. If possible, install a water alarm and a sump pump with battery backup. Stockpile plywood, plastic sheeting, sandbags and other emergency materials, too.

Create a video or list of your belongings and put it with any receipts to prove their value. Store it in a waterproof safe or container with other important financial documents and keep it with your emergency evacuation supplies. This will help with the insurance claims process.

Ready Your Pet

Don’t forget to take precautions to keep your furry, scaled and feathered family members safe during an emergency, too!

Create an emergency supply kit just for your pet with at least three days’ worth of food and water, medications and medical records (in a waterproof container), garbage bags, a picture of your pet in case you become separated, a leash, crate/carrier and anything else necessary for your pet’s survival.

During a storm, bring your animals inside and close to you. Dogs and cats can get confused and become disoriented during difficult times and might try to hide or run away. If necessary, keep dogs in a room with the door closed, cats in a carrier and small animals safely in their cages.

Pets are not always allowed in emergency shelters, so keep a list of places you can bring them in case of a natural disaster. Consider pet shelters, pet-friendly hotels and homes of relatives or friends outside the affected area. American Kennel Club Pet Disaster Relief is a great resource.

It is a good idea to have your dog or cat microchipped. Even an ID tag or collar can be lost or pulled off. A registered microchip might be the only way to be certain your pet can be identified during a disaster. You may also want to apply a pet rescue alert sticker to your window to inform rescuers and first responders that animals could be trapped inside.

Did you know that you can add your pet to your AAA membership? With the complimentary AAA Pet ID Tag Program, AAA can help safely reunite lost pets with their owners. Drop by your local AAA branch to sign up. Learn more.

The Ins and Outs of Hurricane Insurance

What to know about the hurricane deductible that is likely on your homeowners policy.

The History of Hurricane Deductibles

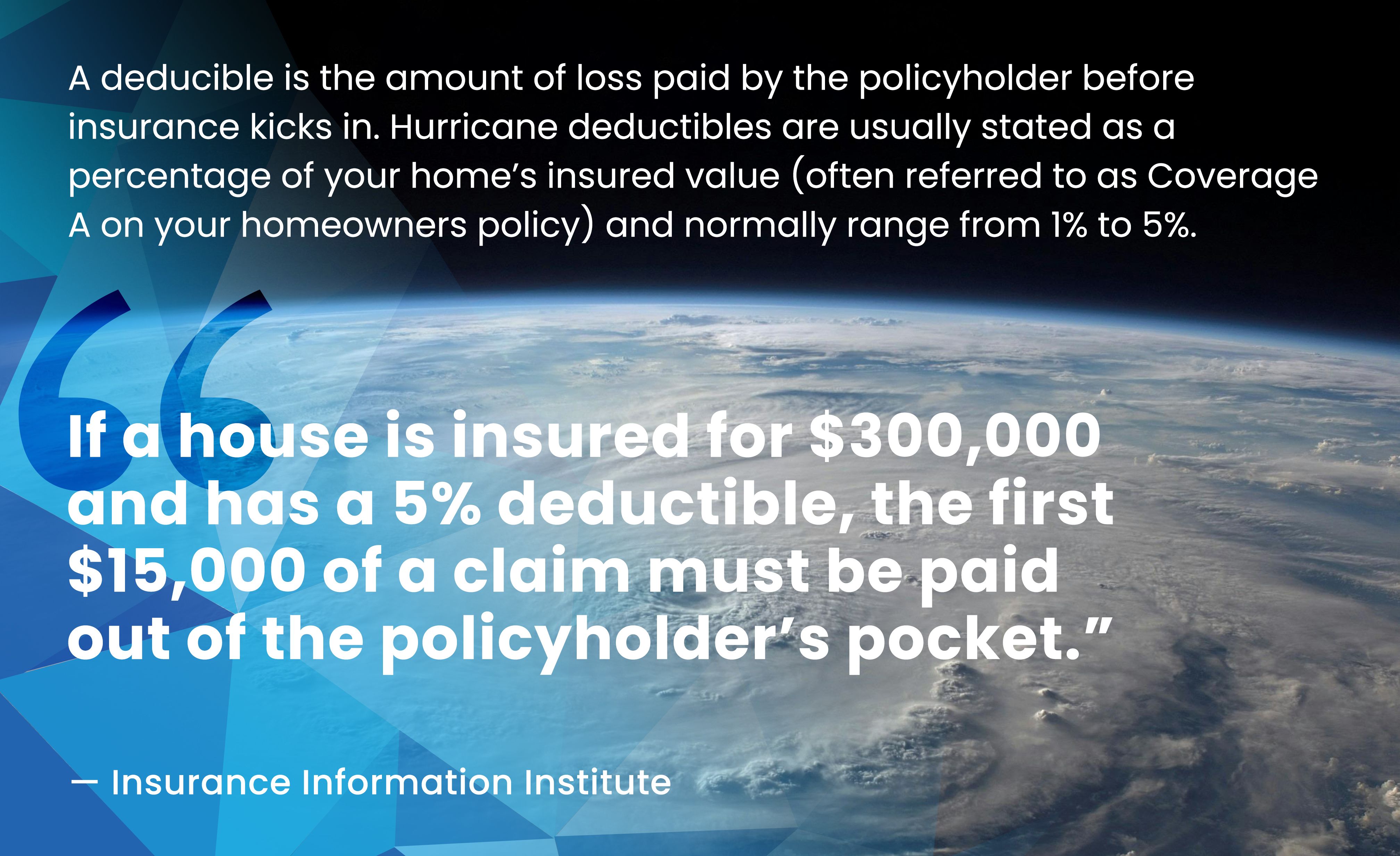

In 1992, Hurricane Andrew left insurers with $15.5 billion in losses – at the time, the costliest hurricane in U.S. history. From that point, hurricane insurance was determined to be a necessity in coastal areas to help cover high-cost property losses due to storm risks like hail and high winds.

“After the wake-up call of Andrew, insurers in many coastal states began to sell homeowners insurance policies with percentage deductibles for storm damage,” according to the Insurance Information Institute. “These deductibles are stated as a percentage of the insured value of the homes and generally are a higher dollar amount than traditional dollar deductibles used for other types of losses such as fire damage and theft.”

Nineteen states and the District of Columbia have hurricane deductibles. In the Northeast, this includes Connecticut, Massachusetts, New Jersey, New York and Rhode Island.

What Is a Hurricane Insurance Deductible?

Homeowners should do the math with their agent to fully understand how much they’re self-insuring for.

Based on where you live, some insurance companies may offer hurricane deductibles stated as higher dollar amounts or possibly no separate hurricane deductible at all. In both cases, this will be reflected in your premium.

When Does Hurricane Coverage Kick In?

There are a few things necessary for hurricane insurance to apply. These triggers vary by state and insurance carrier, but a good indicator comes from the National Weather Service. Once a hurricane watch or warning is issued, the intensity level is crucial. The moment a Category 1 hurricane makes landfall is when the deductible becomes applicable.

More Coverage Options

On its own, your homeowners policy will usually cover loss or damage caused by falling trees on your property due to strong storm winds. And if you are worried about your car, storm damage to your vehicle is also covered as long as you have comprehensive insurance on your auto policy.

Insurance carriers may offer windstorm, named storm and catastrophe deductibles, but keep in mind that your homeowners policy or any kind of storm coverage does not include flood damage. Flood insurance must be purchased separately.

Adding extra wind, flood or storm coverages to your homeowners policy may be worth it for you, or even necessary, depending on where you live. In high-risk coastal areas, the state government or mortgage lenders will likely require it.

Food spoilage coverage is something else to consider ahead of the next big storm. Losses related to power outages are one of the most common insurance claims during hurricane season. Food spoilage coverage may take care of the cost to replace the items in your fridge if your power goes out for a prolonged period.

If you are planning a wedding, fundraiser or other large event during hurricane season, you may also want to purchase special event insurance. In the worst-case scenario that severe weather forces you to cancel or postpone, you will be covered. In the best case, it will be a beautiful day and you will have extra peace of mind knowing that you are protected from other financial losses too, like if your DJ doesn’t show up or someone gets hurt.

Know Your Insurance

When shopping for insurance, always check the financial rating of a company, especially if you live in an area that is prone to hurricanes. Catastrophic weather events result in large swaths of damage that may generate large losses for a particular company and can exceed their ability to pay all the claims.

Each state has its own rules regarding hurricane insurance. Talk to your insurance agent to run through all the technicalities of your policy to make sure you can get the right coverage.

Storm Facts

Do you know your “watch” from your “warning?” Find out in this guide to storm categories and other meteorologist lingo.

Storm Categories

How a storm is classified or described in a weather report is rooted in the strength and severity of the wind.

Dating back to the early 1800s and still used today, the Beaufort scale is a wind measurement tool developed to help sailors gather visual cues about the wind from the water. It goes from zero to 12, with zero being calm and 12 being a hurricane.

A 10 is officially considered a storm on the Beaufort scale, described as having 55 to 63 mph winds, big waves, low visibility and a chance of considerable structural damage. A violent storm (11) is even more intense.

Hurricanes are categorized using the Saffir-Simpson Hurricane Wind Scale. Ranging from 1 to 5, storm categories are based on a hurricane’s maximum sustained wind speed and estimated potential property damage. While all hurricane-force winds are considered dangerous, categories 3 to 5 are known as “major” hurricanes.

When you hear major storm terms in the forecast, it’s time to take action to protect your home, car and belongings, and in the worst cases, evacuate from the area. Hurricane-force winds and storm surges can be deadly.

Category 1: Sustained winds of 74 to 95 mph. Very dangerous. Winds can potentially cause damage to roofs, vinyl siding, gutters and shingles. Large branches may snap, and trees may topple. Extensive damage to power lines and poles could result in power outages that may last several days.

Category 2: Sustained winds of 96 to 110 mph. Extremely dangerous. Major roof and siding damage are possible. Large branches will snap and trees will fall, blocking roads. Near-total power outages are expected and could last weeks.

Category 3: Major. Sustained winds of 111 to 129 mph. Devastating damage. Winds could cause major damage to homes including roof removal. Trees will be snapped and uprooted, blocking roads. Electricity and water will be unavailable for several days to weeks after the storm.

Category 4: Major. Sustained winds of 130 to 156 mph. Catastrophic damage. Severe damage to homes, with potential to lose most of the roof and/or exterior walls. Most trees will be snapped or uprooted and power poles downed. Power outages may last weeks and possibly months. Most of the area could be uninhabitable for weeks or months.

Category 5: Major. Sustained winds of over 157 mph. Catastrophic damage. A high percentage of framed homes will be destroyed with total roof failure and wall collapse. Fallen trees and power poles will isolate residential areas. Power outages can be expected to last for weeks to months. Most of the area will be uninhabitable for weeks or months.

More Storm Terms

Eye/Eyewall: The eye of a storm is its relatively calm center. The eyewall is the dense ring of clouds that surrounds the eye and contains the highest winds.

Doppler: A radar tracking system that sends out energy signals from an antenna to detect the location and velocity of a storm in the atmosphere.

Gale Winds: Sustained surface winds of 39 to 46 mph, strong enough to create high waves and break twigs off trees. At 47 to 54 mph, severe gale winds are more powerful and may cause some structural damage.

Named Storm: A storm or other catastrophic weather event that has been identified and named by the U.S. National Weather Service, the U.S. National Hurricane Center or the U.S. National Oceanic and Atmosphere Administration. Since the 1950s, hurricanes and tropical storms have been given names to quickly identify and communicate them. The naming procedure, established by the World Meteorological Organization, is based on six lists of 21 male and female names on a six-year rotation. The only exceptions to the process are if a storm is so deadly and costly that a future storm of the same name would be inappropriate or if more than 21 named storms happen in a season; in these cases, a separate list of names is used.

Storm Surge/Tide: An abnormal rise in sea level that accompanies a tropical storm system. When a storm surge combines with the normal tide, it is called a storm tide.

Single Cell/Multicell/Supercell Thunderstorms: An explanation of common thunderstorms from the National Severe Storms Laboratory.

- Single Cell – Small storms that grow and die within an hour or so. Often experienced on hot summer afternoons, they produce heavy rain and lightning.

- Multicell – This system could last for many hours and has the potential to produce hail, strong winds, brief tornados and/or flooding.

- Supercell – A long-lived (greater than one hour) storm that is tilted and rotating. It can grow as large as 10 miles in diameter and up to 50,000 feet tall. It only needs to be present for 20 to 60 minutes before a tornado could form. Most large and violent tornadoes come from supercells.

Squall Storm: A group of storms arranged in a line that can be hundreds of miles long, but typically are not very wide. High wind, heavy rain and snow are signatures of these types of storms, which tend to pass quickly.

Tropical Storm: A rotating, low-pressure weather system that originates over warm, tropical oceans with maximum sustained surface winds of 39 to 74 mph. Once winds exceed 74 mph, it is a hurricane.

Watch/Warning/Advisory: While they sound similar, each of these storm alerts means something completely different. Here is how the U.S. National Weather Service breaks them down:

- Advisory – Issued when hazardous weather is occurring, imminent or likely. Used for less-severe weather conditions where caution is advised.

- Watch – A weather threat is possible within 48 hours. Issued when the risk of a hazardous weather event has increased significantly, but exactly when or where it will happen is still uncertain. A watch is intended to provide enough lead time to start thinking about a plan of action or begin executing it if needed.

- Warning – A weather threat is expected within 36 hours or less. Issued when hazardous weather is occurring, imminent or likely. Conditions pose a threat to life or property. People in the path of the storm should take protective action.

What to Do

- If a tree falls on your home due to strong winds, evacuate immediately, make sure everyone is safe and call 911. If you can do so safely, cover up any openings caused by the fallen tree with a tarp or something similar.

- Document the extent of the wind damage by taking photos or videos and make a list of any broken items, being sure to note any structural issues. Then, contact your insurance company as soon as possible to initiate the claims process. After your claim has been filed, the insurance company will typically send an adjuster to assess the damage in-person and repair estimates will need to be given from qualified contractors. This helps ensure that your settlement amount aligns with the actual cost of repairs.

- Work closely with your insurance company to complete the necessary paperwork and fulfill any additional requirements during the claims process. Keep track of all communications and documents related to the claim, in case it’s necessary to reference them in the future.

Are You Covered?

Standard homeowners insurance policies provide coverage for damage caused by wind, including if a tree hits your home or other insured structure, but the extent of coverage may vary depending on the specific terms and conditions outlined in your policy. It’s important to review your insurance policy carefully to understand the scope of coverage for wind-related hazards.

In some cases, the destruction may be so bad that your home could be deemed unsafe to live in. Your homeowners insurance may help to cover the additional living expenses if you need to reside somewhere else while repairs are being made.

If wind has caused damage to your vehicle, such an incident would be covered under the comprehensive portion of your auto insurance policy.

What to Do

- The safety of you and your family is top priority. If flooding is severe, evacuate immediately and seek higher ground. It’s also wise to avoid walking or wading through floodwaters as they can contain hazardous materials and pose dangers you may be unable to see.

- Document damage and notify your insurance provider right away. Although it may seem like a good idea to start cleaning up as soon as possible, it’s best to document the extent of the damage before anything else. Take photos and videos of affected areas to provide evidence for insurance claims.

- Clean, dry and disinfect. Remove standing water by using pumps and wet/dry vacuums and dispose of damaged items that cannot be salvaged. To prevent mold growth, thoroughly dry the affected areas by running dehumidifiers and fans until no sign of moisture is present. Once dried, disinfect all surfaces, furniture and small items to eliminate any potential toxins from the floodwater.

- Water is corrosive and can cause irreversible damage to the structural integrity of your home. Look for signs of damage to the foundation, walls and support structures, especially, but all areas should be inspected as a precaution. If you have concerns about the safety of your home, consult with a professional to evaluate further.

To prevent and reduce future flood damage, consider:

- Elevating electrical outlets, switches and wiring to at least 1 foot above the expected flood level.

- Installing a sump pump.

- Properly sealing and insulating cracks in the home’s foundation or walls.

- Installing water alarms.

- Ensuring proper drainage in and around the property.

Are You Covered?

While standard homeowners insurance may cover some water damage, flooding is covered only by purchasing a separate policy.

If you don’t live in a Special Flood Hazard Area, defined by FEMA as having a 1% or greater chance of flooding in any given year, you’re not federally required to have flood insurance. However, your mortgage lender may still ask you to have it.

As flash floods become more common in the Northeast, flood insurance is still recommended, even if it’s not mandated. It doesn’t need to be a hurricane – or even a coastal area – for flooding to happen. Floods can be caused by rain, storm surges and overflows of water systems and can develop slowly or very quickly without warning.

More than 40% of flood claims come from properties outside high-risk flood zones, according to FEMA.

Mold caused by sudden certain types of storm damage may be covered by your homeowners insurance, depending on what’s listed in your policy. It’s always best to check with your agent if you are unsure about the extent and limits of your coverage.

- Depending on the weather, try to stay as warm or as cool as possible.

- Keep flashlights and extra batteries on hand. Crank or solar-powered lanterns are also great, safe sources of light.

- Unplug major appliances and devices (except the refrigerator), in case of a power surge, which could cause damage.

- Conserve your phone battery, in case you need to use it for an emergency. Consider buying a portable charger and make sure it’s ready for times like these.

- Install smoke and carbon monoxide detectors with battery backup on all levels of your home.

- If using a generator, keep it outside and away from windows.

- Maintain the temperature of your refrigerator or freezer by keeping the door closed as much as possible. Once power is restored, check all your refrigerated foods for freshness; if there is any doubt, throw it out!

Are You Covered?

Check with your insurance agent to see if you have food spoilage coverage on your homeowners policy.

Home Insurance Quote

AAA Insurance has competitive rates, discounts, and knowledgeable agents to get you the right coverage, at the right price. Fill out the form below to receive a quote.

Helpful AAA Resources